How Does U.S. Dollar Strength Impact Global Markets and Investment Performance?

Across the global currency landscape the U.S. Dollar (“USD”) is one of the most influential currencies and can be a key factor in driving how other global markets and assets perform. Before we dive into these relationships, I think it would be important to look at what primary underlying factors influence the value of the USD which include:

- Interest rates

- Inflation

- Economic health

- Global Safe Haven Status

- Trade policies

While all the above factors are important in influencing the USD’s value, a key factor we will focus on in this blog is U.S. interest rates, and more specifically the federal funds rate, and its recent trends. The federal funds rate, is the target interest rate range set by the Federal Reserve and it directly influences the USD’s global valuation through capital flows, investment yields, and borrowing costs.

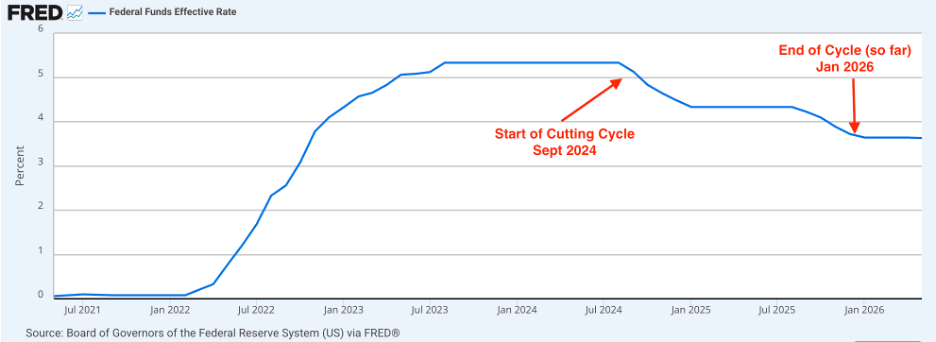

Looking at the USD’s price trend, a lot of the recent relative weakness in the USD can be attributed to when the Fed started the last rate cutting cycle back in September 2024. During the cycle the Fed cut rates six times, with the last cut coming in December 2025, and over this time frame the USD trended lower as well. The cycle may not be over yet, but for the moment we will call this the end of the last cutting cycle.

The market, most assets, currencies, etc. are forward looking instruments that price-in updated information immediately. If we look at the DXY index chart below, which tracks USD’s value, the index actually started to decline in July 2024 before the September rate cut was announced. This is due to the market pricing lower interest rate expectations in advance to the September 2024 Fed meeting, which as discussed previously led to a decline in the USD.

Since the last rate cut in December 2025, the Fed has kept rates steady. This has helped the USD stabilize and even rebound slightly higher over the past several months. The Fed’s new Chair, Kevin Warsh, also started in May of 2026, and while he has not explicitly communicated that his policy stance will be to keep rates high he did allude to the fact that he will take a tougher stance on inflation which can be inferred as fed funds rate expectations are likely to remain higher for longer. These developments have helped fueled the DXY index higher and it has rebounded to 101.2 and is now above its 10 year average of 98.6.

Asset Performance

So how does the federal funds rate impact asset pricing? A higher fed funds rate yield can attract capital inflows from foreign investors, which then drives up global demand for that country’s currency. For instance, when the fed funds rate increases, yields on U.S. fixed income assets (like Treasury bonds) generally increase. This typically makes holding USD denominated assets more attractive to global investors.

The fed funds rate also sets the baseline for the cost of capital across different assets. As we mentioned previously short-term debt, cash, and fixed income bonds’ yields are directly affected by changes in the key rate’s level. Equity prices can be fundamentally derived by asset pricing valuation models that use a discount rate in the denominator of their valuation framework. When rates change this directly affects equity valuations and therefore prices; higher rates typically mean lower valuations due to a higher denominator and can lead to lower prices.

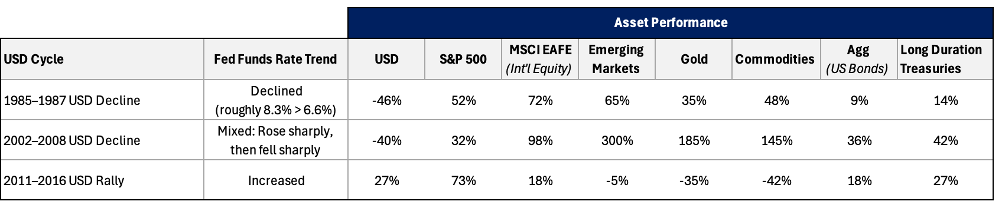

Now connecting this back to how the USD effects asset prices, lets first look at how USD performance typically mirrors historical trends in the federal funds rate. The below table’s data set looks at three time periods. Two out of the three periods reflect this assumption: both data points exhibited weaker trends during 1985-1987 and stronger trends for the 2011-2016 period. The 2002-2008 period had a mixed result, most likely due to being skewed by the Dot Com Bubble and Great Financial Crisis recessions.

In all cases where the USD declined, U.S. equities underperformed international equities and emerging markets. This makes sense as typically a major component of return for foreign equities is attributed to their relative currency return effects. Thus even though U.S. equities were positive in these weaker USD periods, its return lagged foreign equities due to the weaker relative currency effects.

Looking at the other asset classes we can conclude from our limited data set that real assets such as gold and commodities had a negative return when the USD strengthened and vice versa when it weakened. Bonds appear to have no relationship with USD effects as they had a positive return across all periods.

How to Mitigate USD Effects in Portfolio Construction

It is prudent to have a diversified portfolio that is not only diversified by asset class, but also by different types of risk exposures. Owning assets like international equities can help reduce the impact to the portfolio when the USD declines and U.S. equity performance lags international equities.

Also, when the USD declines, owning hard assets may serve as a good portfolio protection hedge. At Wiser, we personally do not allocate to hard assets such as gold and commodities. However, some of our model portfolios do have exposure to digital assets which we believe this asset class carries similar attributes and that they can also serve as a hedge to a decline in the USD value.

Ultimately, the goal of portfolio construction is to mitigate risk factors as much as possible and to create a diversified portfolio that maximizes your risk adjusted return, or return per unit of risk taken.

Reach out to schedule a complimentary consultation today, if you would like to learn more about the US dollar and how it can shape your financial portfolio.

Andrew Pratt, CFA, CBDA

Director of Investments, Wiser Wealth Management

Share This Story, Choose Your Platform!

Wiser Wealth Management, Inc (“Wiser Wealth”) is a registered investment adviser with the U.S. Securities and Exchange Commission (SEC). As a registered investment adviser, Wiser Wealth and its employees are subject to various rules, filings, and requirements. You can visit the SEC’s website here to obtain further information on our firm or investment adviser’s registration.

Wiser Wealth’s website provides general information regarding our business along with access to additional investment related information, various financial calculators, and external / third party links. Material presented on this website is believed to be from reliable sources and is meant for informational purposes only. Wiser Wealth does not endorse or accept responsibility for the content of any third-party website and is not affiliated with any third-party website or social media page. Wiser Wealth does not expressly or implicitly adopt or endorse any of the expressions, opinions or content posted by third party websites or on social media pages. While Wiser Wealth uses reasonable efforts to obtain information from sources it believes to be reliable, we make no representation that the information or opinions contained in our publications are accurate, reliable, or complete.

To the extent that you utilize any financial calculators or links in our website, you acknowledge and understand that the information provided to you should not be construed as personal investment advice from Wiser Wealth or any of its investment professionals. Advice provided by Wiser Wealth is given only within the context of our contractual agreement with the client. Wiser Wealth does not offer legal, accounting or tax advice. Consult your own attorney, accountant, and other professionals for these services.