Investment Compounding Explained: How It Works and Why It Matters

A penny saved is a penny earned is an adage that is commonly attributed to Benjamin Franklin. The saying encourages frugality and suggests that even the smallest amount of savings today can amount to meaningful wealth over time.

While saving for a goal, let’s say retirement, is a good habit to practice, it is only one piece of the puzzle. While the security of saving money under a mattress, or in a low yielding bank savings account sounds nice on the surface, we should also want our money to “work” for us through the power of compounding. What if we invested a portion of our savings in the stock market instead and have our wealth compound at a much higher rate?

What is Compounding and an Example

Compounding expresses the idea that when we invest money, we actually make money not only on the initial amount invested, but also on the additional growth from that investment’s return.

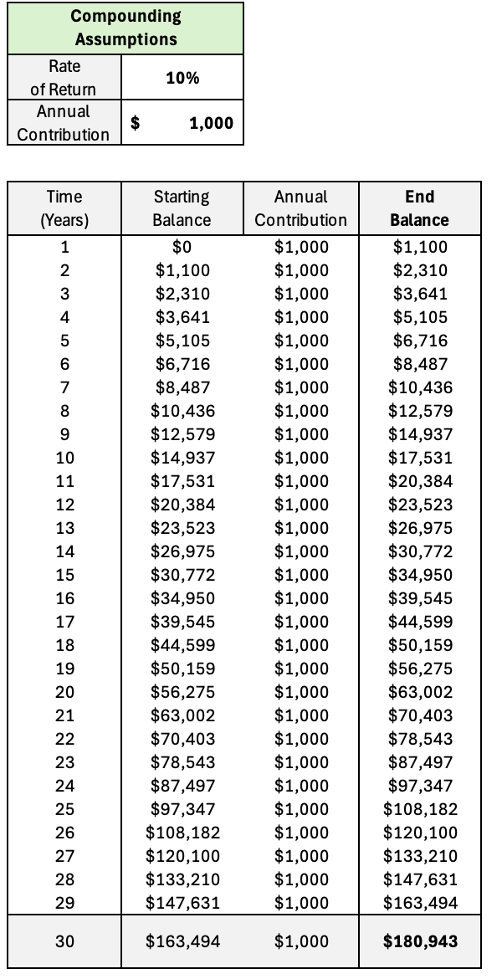

For example, if you invest $1,000 with an annual return of 10% the investment would receive $1,100 at the end of year one, so $100 extra. In year two, if you make another 10% return on the same $1100 investment form the first year, you would receive $110 extra leading to a new total balance of $1,210. Over time this compounding effect makes a huge difference, especially the longer your investment time horizon.

The graph below assumes an annual $1,000 investment at a 10% rate of return. The rate of return assumption is equivalent to the S&P 500 index’s return over the past 65 years. The chart below shows a 30-year time period. At the end of this period your investment would have resulted in a compound return of $180,943. Compare this to the $30,000 you would only have if you just saved $1,000 every year for 30 years. Now that is a big difference!

Benefits of Compounding

I believe there are two primary reasons why we should want to invest and have our assets compound over time. The most obvious reason that we alluding to previously is that compounding greatly accelerates wealth accumulation, especially as your time horizon increases. In the example above if our time horizon was only 20 years, then the investment would have grown to $63,002. However, if we were able to wait 10 more years, then this amount would have almost tripled and have grown to $180,943.

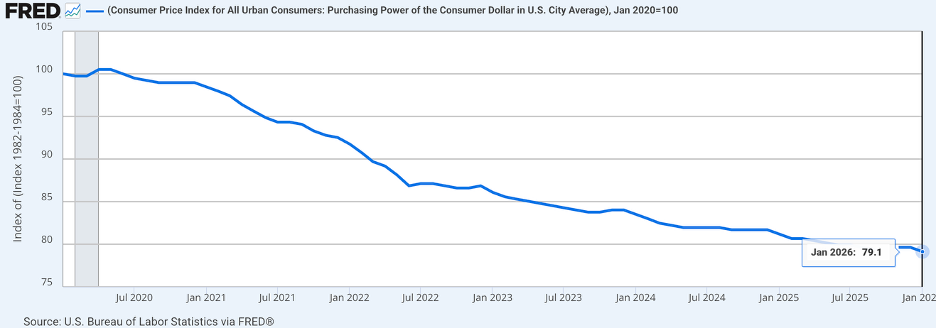

The second reason is that we want to maintain our purchasing power above inflation. The U.S. Federal Reserve’s inflation target historically has been between 2-3%. This may not sound like a lot but over time this greatly adds up. Looking at the chart below, we can see that the U.S. Dollar has lost roughly 21% of its purchasing power over the past 6 years! Traditional bank savings accounts typically pay a yield on deposits that is very low and predominately much lower than the inflation rate. The return differential between equity returns and inflation compounds over time. Not only does this lead to significantly higher real wealth, but it also mitigates inflation risks by protecting your purchasing power over time.

https://fred.stlouisfed.org/series/CUUR0000SA0R

Reach out to schedule a complimentary consultation today, if you would like to learn more about how compounding interest can work for you.

Andrew Pratt, CFA, CBDA

Investment Manager, Wiser Wealth Management

Share This Story, Choose Your Platform!

Wiser Wealth Management, Inc (“Wiser Wealth”) is a registered investment adviser with the U.S. Securities and Exchange Commission (SEC). As a registered investment adviser, Wiser Wealth and its employees are subject to various rules, filings, and requirements. You can visit the SEC’s website here to obtain further information on our firm or investment adviser’s registration.

Wiser Wealth’s website provides general information regarding our business along with access to additional investment related information, various financial calculators, and external / third party links. Material presented on this website is believed to be from reliable sources and is meant for informational purposes only. Wiser Wealth does not endorse or accept responsibility for the content of any third-party website and is not affiliated with any third-party website or social media page. Wiser Wealth does not expressly or implicitly adopt or endorse any of the expressions, opinions or content posted by third party websites or on social media pages. While Wiser Wealth uses reasonable efforts to obtain information from sources it believes to be reliable, we make no representation that the information or opinions contained in our publications are accurate, reliable, or complete.

To the extent that you utilize any financial calculators or links in our website, you acknowledge and understand that the information provided to you should not be construed as personal investment advice from Wiser Wealth or any of its investment professionals. Advice provided by Wiser Wealth is given only within the context of our contractual agreement with the client. Wiser Wealth does not offer legal, accounting or tax advice. Consult your own attorney, accountant, and other professionals for these services.