Understanding Risk Tolerance

")

What exactly is risk tolerance? By definition, it is the measure of an investor’s willingness to accept risk. Understanding your risk tolerance is essential to understanding how much loss you can stomach during a stock market downturn. Wiser Wealth Management’s portfolio advisor, Brad Lyons, explained the concept of loss aversion and how investors feel more pain from losses than the joy of capital gains in a recent blog. Understanding your risk tolerance helps determine the type of allocation that an investor should maintain in their portfolios.

Advisors attempt to understand an investor’s tolerance through certain risk questionnaires. The questionnaires ask various questions, for example, if an investment drops below 20% in your portfolio, how would you react? The answer choices are usually stay invested, sell your investments to get out of the market or invest more. They can also include some similar to when you make financial decisions to invest, what are you concerned with? The answers could be growth, income, or just maintaining principal. One of the final questions is typically about when you will need the investments, or what is your time horizon? As a rule of thumb, a younger investor would have a more aggressive allocation because they have a longer time to invest and more time to recover should the market drop. Usually, a retiree will have a more conservative portfolio in retirement.

An example of an aggressive portfolio may be 90/10, or 90% equities and 10% fixed income while a conservative portfolio may be 30/70, or 30% stocks and 70% fixed income. However, sometimes there is a difference between the risk tolerance of the individual and the actual risk capacity they are able to withstand.

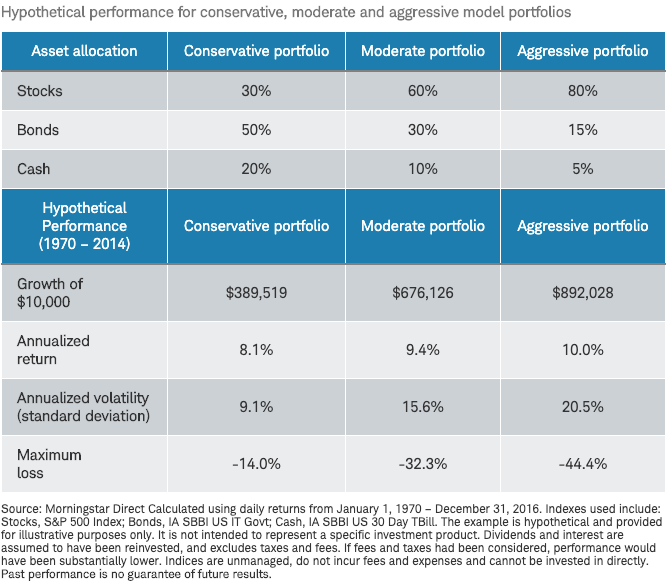

The below example from Charles Schwab shows the hypothetical performances for a conservative, moderate and aggressive portfolio.

At Wiser Wealth Management, we assess client risk tolerance through a risk profile software called FinaMetrica. In the initial consultation meeting, we send investors a 25-question questionnaire. We also resend the questionnaire annually before each review meeting to help identify and maintain individual risk tolerance ranges. For example, if an investor’s risk number is in a higher risk range, they will usually be allocated toward a more aggressive portfolio meaning more stocks or growth assets, than bonds or fixed income assets.

It is important to realize that investors do not usually fully participate in the market. Investors may watch CNBC and see red tickers flash across the screen showing the S&P or “market” losses for the day, current quarter or year-to-date. However, most portfolios are not invested 100% into the S&P 500. A well-diversified portfolio will consist of a blend of equities, both domestic and international, as well as bonds, whether they are corporate, international, emerging market or even U.S Treasury. At Wiser Wealth Management, we use a tactical approach to portfolio management developed through low cost ETFs.

We are a fee-only financial planning firm and focus not just on the investments, but how they fit into your overall financial plan. We stress test portfolios and financial plans to prepare for both the good and bad periods that markets experience. We plan for not if, but when, there are volatile times. Unless a client’s financial goals or life priorities have changed, we maintain the course and remain invested as planned. If you would like a second opinion on your portfolio and how it incorporates into your overall financial plan, please feel free to reach out to us.

Matthews Barnett, CFP®, ChFC®, CLU®

Financial Planning Specialist

Posted 4/23/2020

Share This Story, Choose Your Platform!

Wiser Wealth Management, Inc (“Wiser Wealth”) is a registered investment adviser with the U.S. Securities and Exchange Commission (SEC). As a registered investment adviser, Wiser Wealth and its employees are subject to various rules, filings, and requirements. You can visit the SEC’s website here to obtain further information on our firm or investment adviser’s registration.

Wiser Wealth’s website provides general information regarding our business along with access to additional investment related information, various financial calculators, and external / third party links. Material presented on this website is believed to be from reliable sources and is meant for informational purposes only. Wiser Wealth does not endorse or accept responsibility for the content of any third-party website and is not affiliated with any third-party website or social media page. Wiser Wealth does not expressly or implicitly adopt or endorse any of the expressions, opinions or content posted by third party websites or on social media pages. While Wiser Wealth uses reasonable efforts to obtain information from sources it believes to be reliable, we make no representation that the information or opinions contained in our publications are accurate, reliable, or complete.

To the extent that you utilize any financial calculators or links in our website, you acknowledge and understand that the information provided to you should not be construed as personal investment advice from Wiser Wealth or any of its investment professionals. Advice provided by Wiser Wealth is given only within the context of our contractual agreement with the client. Wiser Wealth does not offer legal, accounting or tax advice. Consult your own attorney, accountant, and other professionals for these services.