Ways to Minimize Taxes in Retirement

We have all heard the saying, “the only guarantees in life are death and taxes.” Even though paying taxes is unavoidable, there are ways to help reduce their impact—especially during retirement. By proactively pre-planning, you can better implement tax-efficient withdrawal strategies, depending upon where your money is invested. Unlike previous generations, most clients planning to retire in the next ten, twenty, or thirty years, will not expect to live on a pension provided by their employer. Living off of personal savings and social security during retirement has become the norm for most people. To build up the necessary funds, then, most people pay into a 401k, Roth 401k or Roth IRA over the course of their careers. Although it is nice having different options, the tax requirements for these accounts are complex and can vary widely from each other. So, which one should you be contributing to? Let’s breakdown the options to get a better idea of their unique offerings and requirements.

What happened to pensions?

Since the reduction in the number of pensions across America, the popularity of the 401k has increased exponentially. The savings scheme was created after Congress signed the Revenue Act of 1978 that included a provision in the Internal Revenue Code—Section 401k—which deferred taxation of an employee’s compensation. In 2006, the Roth 401k was created from the Economic Growth Tax Relief Reconciliation Act of 2001. Originally, the ability to contribute to a Roth 401k was supposed to sunset in 2010, but the Pension Protection Act of 2006 allowed it to remain intact.

Considering a Traditional 401k

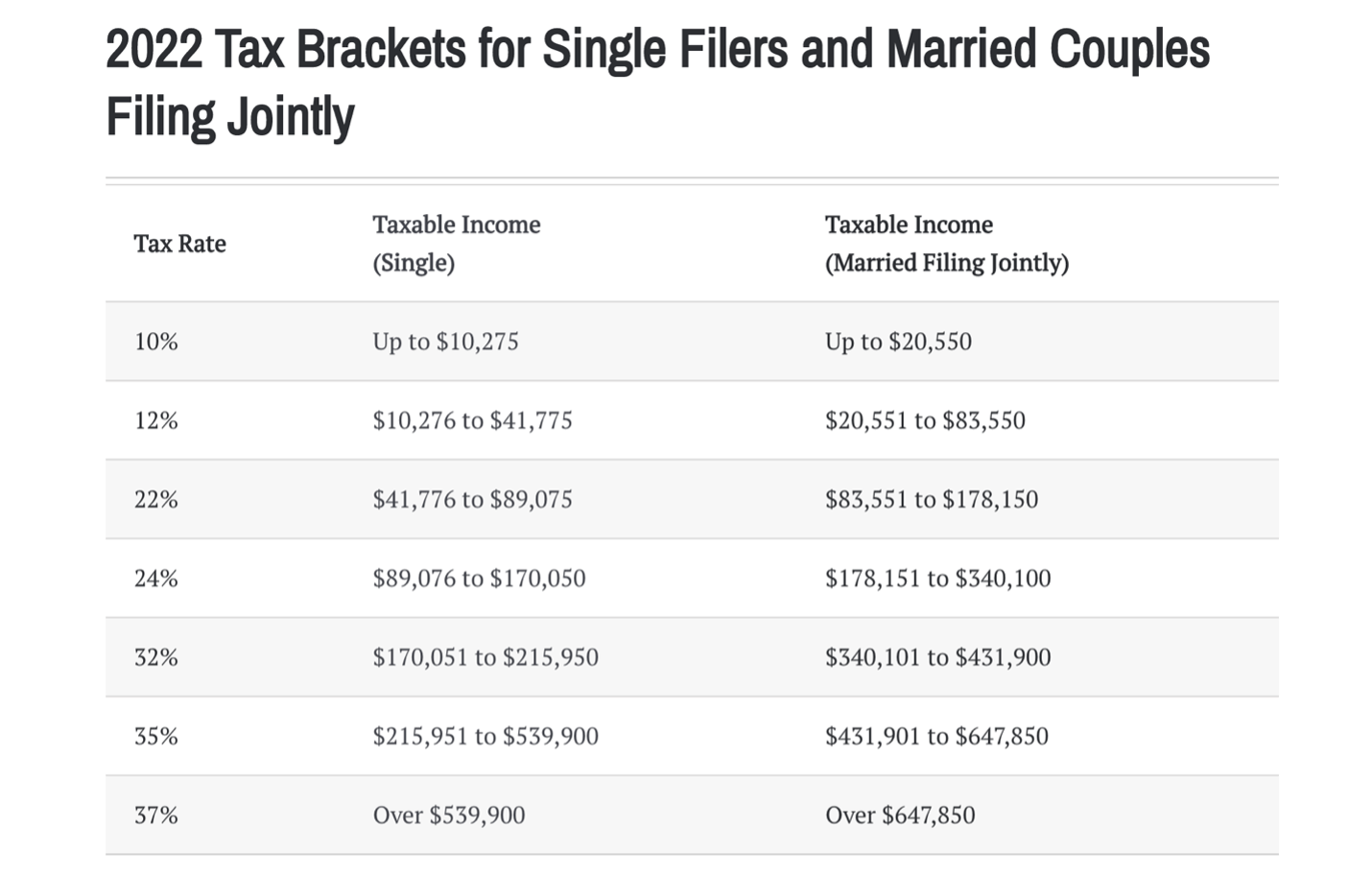

The main differentiator between the Traditional and Roth is the timing of the tax benefit. A traditional 401k contribution is made with pre-tax dollars, and then you pay ordinary income taxes on the withdrawal in retirement. Because this is a deduction from your paycheck, it can allow you to reduce your taxable income during the years you are working. A couple of other features to keep in mind as you consider a traditional 401k. First, employee matching contributions are also made pre-tax, and, second, contributions grow tax deferred. Eventually, however, the IRS would like all that money you spent years deferring. Therefore, they created what is called the Required Minimum Distribution or “RMD.” The RMD amount is determined by the account’s balance as of the previous year end times a percentage that is calculated from life expectancy tables. The percentage for a 72-year-old comes out to just under 4% for 2020. Previous to 2020, the RMD age was 70 ½. However, due to the recently passed SECURE ACT (Setting Every Community Up for Retirement Enhancement) signed in December of 2019, the age was pushed back to age 72 as long as you turned 70 1/2 after January 1, 2020. There is also now legislation trying to get passed under Secure Act 2.0 which would increase the RMD requirement further out to age 75.

Roth 401k vs Roth IRAs

The Roth 401k, on the other hand, is contributed with after-tax dollars. The earnings are tax free as long as the investor has reached age 59 ½. The Roth 401k is also subject to RMDs (although not taxed) but this can be avoided if the funds get rolled over into a Roth IRA in retirement.

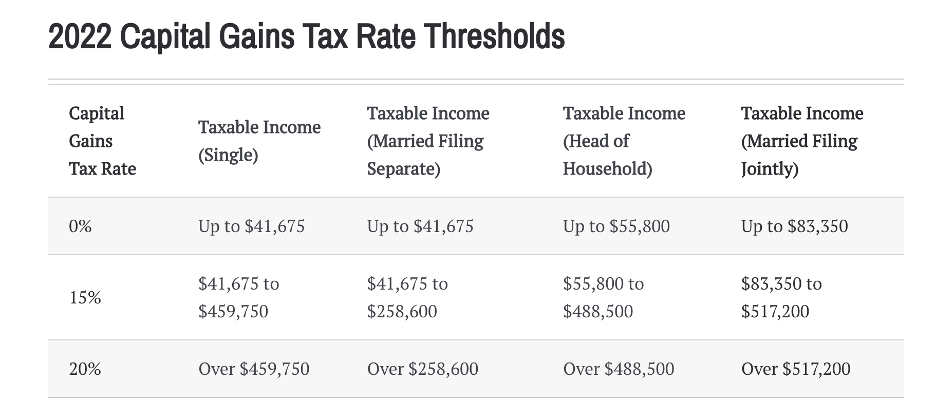

Roth IRAs are individual retirement accounts opened outside of your employer plans. They are contributed to with after-tax dollars, but they differ slightly from Roth 401k in that their contribution limits by the IRS are lower at $6,000 ($7,000 if age 50 or older) and they do not require RMDs. The entire amount of the account can be passed down tax free as well. However, as shown in the graph below, if you are single and make over $144,000 (or if married over $214,000) then Roth IRA contributions are not allowed.

There is a way to sidestep the income limits on Roth IRAs through what’s called the “Back Door Roth.” This is where a client contributes money to a Traditional IRA, and then he or she rolls over the funds into the Roth IRA account. In this case, the rollover amount would then be included as taxable income.

Choosing a Traditional 401k or a Roth 401k

So, at this point you might be wondering whether you should choose the traditional 401k over the Roth 401k or vice versa? The decision boils down to your current income status as well as what tax bracket you believe you’ll fall into during retirement. As stated before, the goal of the traditional 401k is to reduce income taxes and participate in tax deferred growth. If not including that income helps you stay below a certain bracket, or if you believe your individual taxes will be significantly lower in retirement, then a traditional 401k could be right for you.

The key, though, is to rollover that investment into a taxable brokerage account each year. Any investor with a single traditional account in retirement, needs to be aware of how much they’ll withdraw as any excessive withdrawals could cause them to move up a tax bracket thus increasing federal social security taxation, as well as Medicare Part B premiums. The current highest marginal income tax bracket is 37%, but in 1981 it was 70% and back in 1963 it was even as high as 91%. While I hope we don’t move that drastically, we have been in historically low brackets given our amount of deficit, especially after COVID. Therefore, taxation policies will most likely increase in the future.

If you are a younger investor, currently in one of the lower tax brackets, or you prefer to pay the taxes during your working years, you might consider choosing a Roth 401k. This could also be a good choice if you believe you will be in a higher bracket in retirement. Also, the Roth 401k could be a good choice if you know you will not require the funds as income in retirement, or you want to leave the remaining balance as a legacy. Roth 401k funds can pass down as a tax-free inheritance.

Combining a Traditional 401k with a Roth 401k

You can also choose a combination. Contributing to both traditional 401k and Roth 401k accounts can be helpful if you are unsure what tax bracket you’ll qualify for in retirement. The maximum contributions allowed between the two is $20,500. If you are over 50, you can catch-up with contributions each year at an additional $6,500. Often, a mix is the best of both worlds because combining both tax free and taxable income in retirement allows you to lower your tax bracket and withdraw enough income to live comfortably.

Reducing Taxes in the Withdrawal Phase

Lastly, there are ways to reduce taxes during the withdrawal phase based on certain spending strategies. Charitable giving either through gifted securities, cash to Donor Advised Funds (if itemized) or through RMDs with qualified charitable distributions (QCDs) can help lower your tax liability. QCDs are also a good year-end way to minimize tax bills as they are a direct transfer of funds from an IRA to a qualified charity. These satisfy the RMD requirement, but it also allows the money to be excluded from taxable income. And they do not require an investor to itemize the donation. In order to qualify, the investor must be at least 70 1/2 and the max that can be distributed is up to $100,000. The receiving charity must be a 501(c)(3) organization and contributions cannot be made to private foundations or transferred into a donor advised fund.

Contributing part of your pre-retirement income to a 401k or Roth 401k or Roth IRA is an essential part of most successful financial plans. Choosing which type of account is appropriate for your situation depends upon a host of factors, including your current and future tax liabilities. If you would like to discuss a tax savings strategy in conjunction with your overall financial plan, please reach out to us at 678-905-4450 or schedule a consultation here.

Have more questions? Contact Us

Matthews Barnett, CFP®, ChFC®, CLU®

Financial Advisor

Share This Story, Choose Your Platform!

Wiser Wealth Management, Inc (“Wiser Wealth”) is a registered investment adviser with the U.S. Securities and Exchange Commission (SEC). As a registered investment adviser, Wiser Wealth and its employees are subject to various rules, filings, and requirements. You can visit the SEC’s website here to obtain further information on our firm or investment adviser’s registration.

Wiser Wealth’s website provides general information regarding our business along with access to additional investment related information, various financial calculators, and external / third party links. Material presented on this website is believed to be from reliable sources and is meant for informational purposes only. Wiser Wealth does not endorse or accept responsibility for the content of any third-party website and is not affiliated with any third-party website or social media page. Wiser Wealth does not expressly or implicitly adopt or endorse any of the expressions, opinions or content posted by third party websites or on social media pages. While Wiser Wealth uses reasonable efforts to obtain information from sources it believes to be reliable, we make no representation that the information or opinions contained in our publications are accurate, reliable, or complete.

To the extent that you utilize any financial calculators or links in our website, you acknowledge and understand that the information provided to you should not be construed as personal investment advice from Wiser Wealth or any of its investment professionals. Advice provided by Wiser Wealth is given only within the context of our contractual agreement with the client. Wiser Wealth does not offer legal, accounting or tax advice. Consult your own attorney, accountant, and other professionals for these services.